Spring 2022

Threat to living standards from inflationary pressures

On Wednesday 23rd March 2022 the Chancellor, Rishi Sunak, presented to Parliament the “Spring Statement” , which was supposed to be a light-touch presentation of the Office for Budget Responsibility’s latest set of forecasts for the economy and public finances. Significant tax or spending changes should now, in theory, be made at the Autumn Budget.

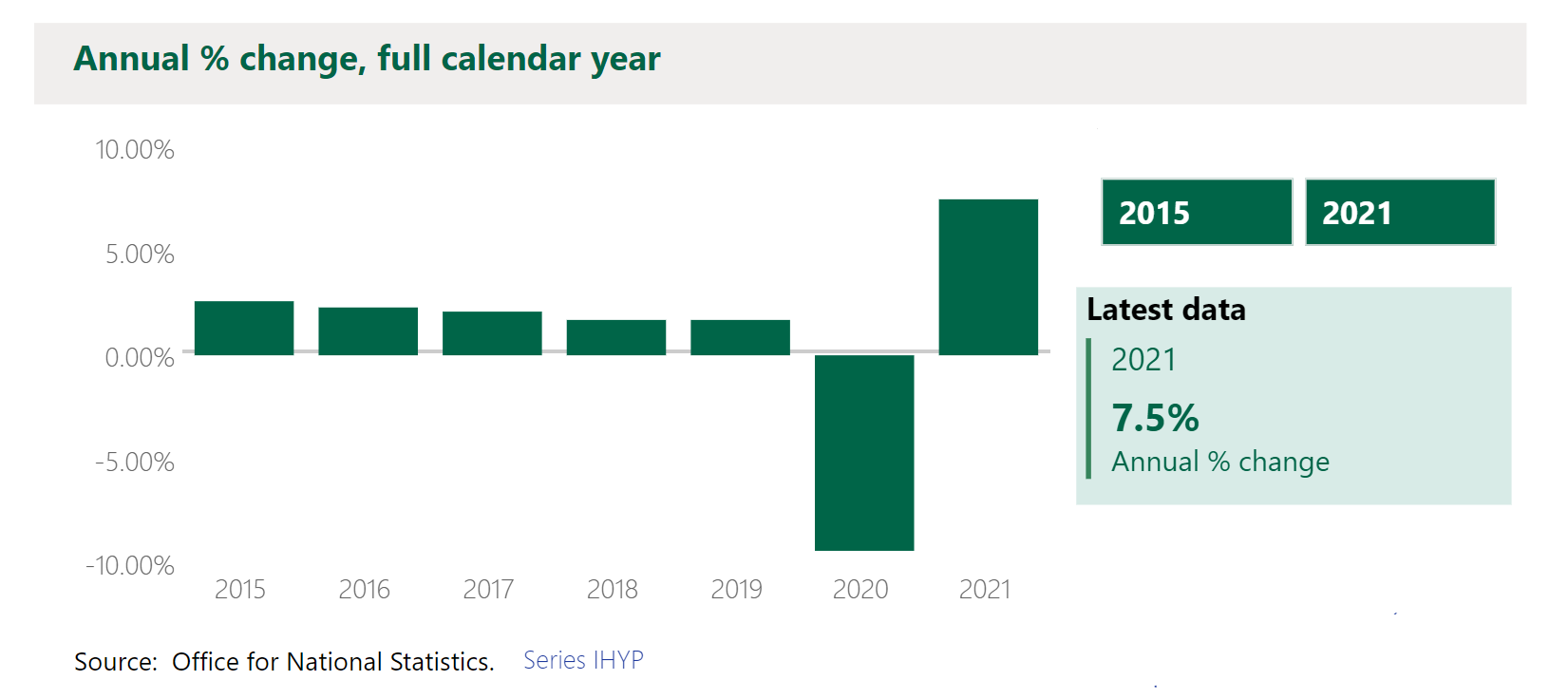

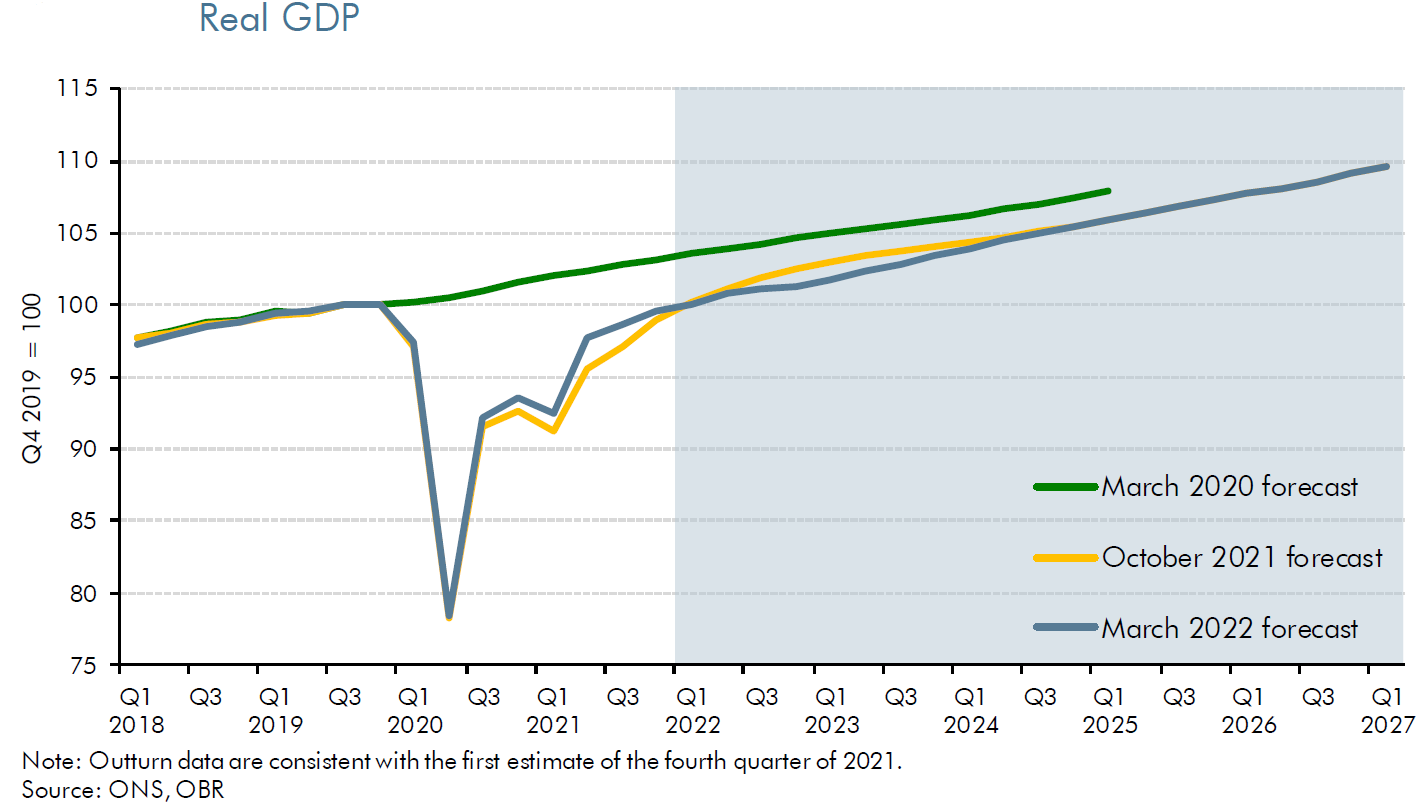

Over 2021, the UK economy rebounded (GDP +7.5%) beyond the OBR’s expectation. Nominal GDP was revised up materially in the UK’s 2021 accounts, to a level around 2 per cent higher than the OBR’s October 2021 forecast in the medium term. The OBR had expected output growth of 6½% for last year (2021), whereas the ONS are currently reporting around 7½%. Putting the UK economy back to being the same size in terms of output, as the pre-pandemic level. Much earlier and stronger than the OBR had been projecting during the pandemic.

For 2022, in their October 2021 report, the forecast was for GDP growth following the pandemic to be 6% in 2022. That increase in output has now been curtailed owing to current events. The OBR now expect real GDP growth of 3.8 per cent in 2022, down 2.2 percentage points from their October 2021 forecast.

As a comparison to the OBR’s expectation for the forthcoming year, the Treasury’s March 2022 survey of independent forecasts showed an average forecast of 4.4% for 2022.

A key judgement in the OBR’s forecasting is that they see a weak outlook for the growth of households’ real incomes, although this is allied to an expectation that households will cushion consumption by using savings.

The OBR see income growth as being likely to be much lower than they had expected last October – especially in the near term. Perhaps more positively given recent economic history, the OBR believe that business investment will grow rapidly this year and continue to outpace GDP growth.

Before the Russian invasion of Ukraine, economic indicators of business activity in the UK for February 2022 were relatively upbeat. For example, the index from surveying purchasing managers showed strong growth during the month. Growth in the UK service sector accelerated sharply in February 2022, as the Omicron wave of the COVID-19 pandemic subsided, even in in the face of high levels of infection. Set against positive business activity indicators for early 2022 was the fact that UK consumer price inflation (CPI) had already reached a 30-year high, with the distinct, and now almost indisputable prospect of further inflationary pressure to come. Although the UK is not directly involved in the conflict, the uncertain course and duration creates the prospect that energy prices could rise further than markets currently assume.

Russia is one of the world’s largest producers and exporters of oil and gas and an important supplier of gas to many European countries. For example, the average supply for Germany between 2016-2020 was 47%.

Food prices, such as wheat and maize, on international financial markets, have also risen. Russia and Ukraine are important producers of various agricultural products. Russia is a major exporter of fertilisers (around 25% of total world exports).

In 2020, Russia was the EU’s fifth largest trading partner. Some EU banks are reported to have relatively large exposure to the Russian economy. For the UK, the most likely economic effects, at least initially, will come through higher energy prices since Russia is the UK’s 19th largest trading partner.

Inflation

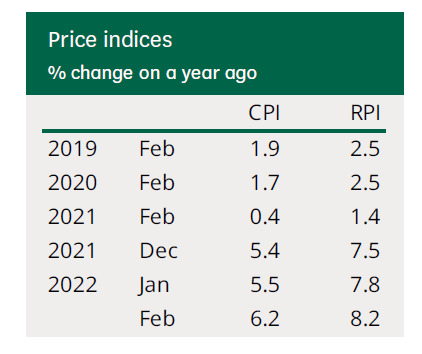

The OBR now expects CPI inflation to peak at close to 9% in the last quarter of this year, 2022. A considerable volte-face on the previous expectation of transitory inflation ‘peaking’ at close to 5%. The duration and persistence of inflation is also likely to be a factor over the near and medium term. For example, the household energy price cap will likely increase by around 50% when next revised again in this coming October 2022.

Consumer price inflation has been rising in many countries since 2021. Pandemic-related supply shortages being the main factor, as the global economy recovers there has been increased demand for consumer goods. With an imbalance between strong demand and disrupted global supply. There have also been higher transportation costs around the world.

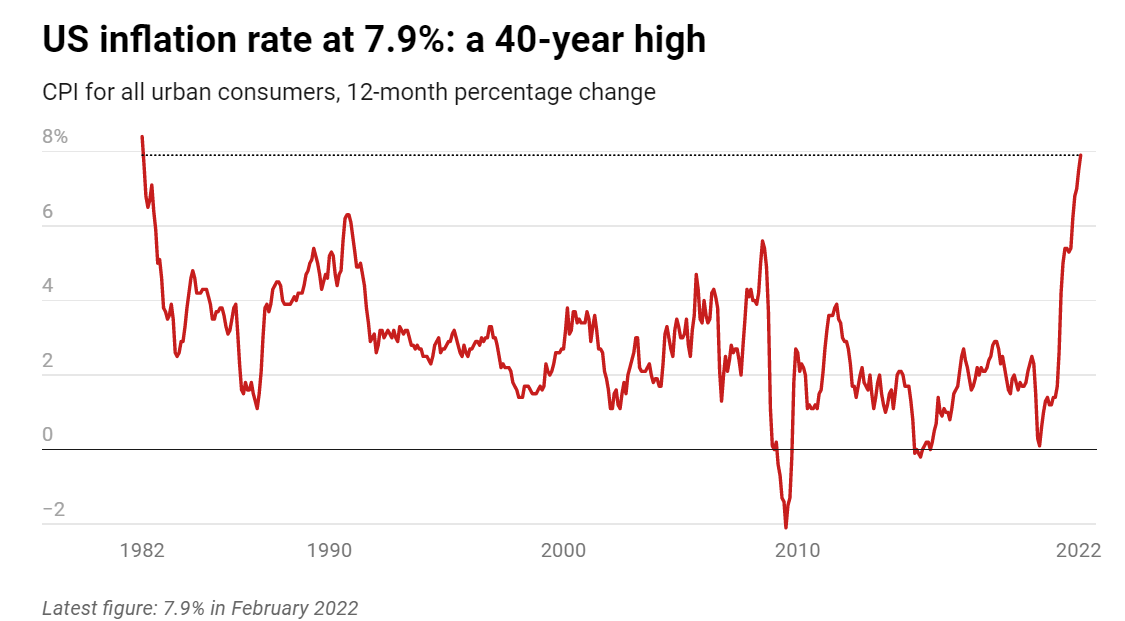

The UK’s inflationary pressures are consistent with European neighbours and notably lower than the US, where CPI inflation is at a 40-year high and rising.

The current energy price shock will have a different effect than that experienced during the 1970s. While the UK is no longer a net exporter of energy, and inflation will likely reduce living standards, the UK economy is less energy-intensive. Notwithstanding this, the UK is dependent on gas for around 30% of supply of electricity generation and to the same extent is a net importer of energy overall, for which market prices are paid. In 2019 the UK relied on gas and oil to meet three-quarters of total energy needs; hence the UK can expect higher gas and oil prices to have a significant impact on the economy.

Labour Market

The continuing good news is that UK unemployment has continued to fall. 32.49 million people were in employment at the end of 2021. Employment was up 380,000 from the year before. The ONS report that while employment levels have risen over the past year, they are still 519,000 below their pre-pandemic level.

The UK unemployment rate is 1.34 million people, a fall of 402,000 from the year before and 39,000 below the pre-pandemic levels.

The number of vacancies continues to increase to reach 1.32 million at the start of this year. Even so, average wages fell in real terms in the three months to January 2022, by around ½% (including bonuses).

An issue identified by the OBR is that the number of people who are economically inactive is increasing. Inactivity levels have risen over the last year and now represent 328,000 persons above the pre-pandemic level.

A lower overall labour supply coupled with continued strength in labour demand, results in a tighter labour market than previously expected last October. This, combined with growing pressures on the costs of living, means the OBR expect stronger nominal earnings growth in the coming year. But not sufficient to keep pace with rising inflation over the next 12 months.

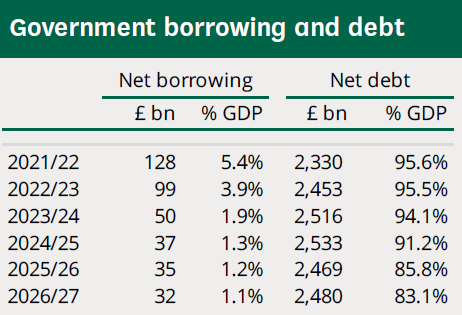

Government borrowing and debt

Public finances have continued to recover more quickly from the pandemic than the OBR have expected. Borrowing in this financial year is expected to come in lower than forecast last October. Tax revenues have held up much better during the pandemic than anticipated, especially among higher-rate income taxpayers and financial companies. Spending has also been revised down.

Even though higher inflation is pushing up debt interest costs, annual borrowing is set to more than halve from the post-World War II high of £322 billion (15% of GDP) in 2020-21, reducing sharply, to £128 billion (5.4% GDP) in 2021-22, £55 billion less than the OBR forecast last October.Borrowing for 2022-23 is projected to be higher at £99 billion and this reflects record-high debt interest costs of £83 billion, rebates and tax reductions, which are expected to offset around half the hit to household finances from the expected higher energy costs and should mitigate pressure on prospective living standards. Future cuts announced to personal taxes should cost £10 billion and will undo around one quarter of the overall value of the personal tax rises previously announced.

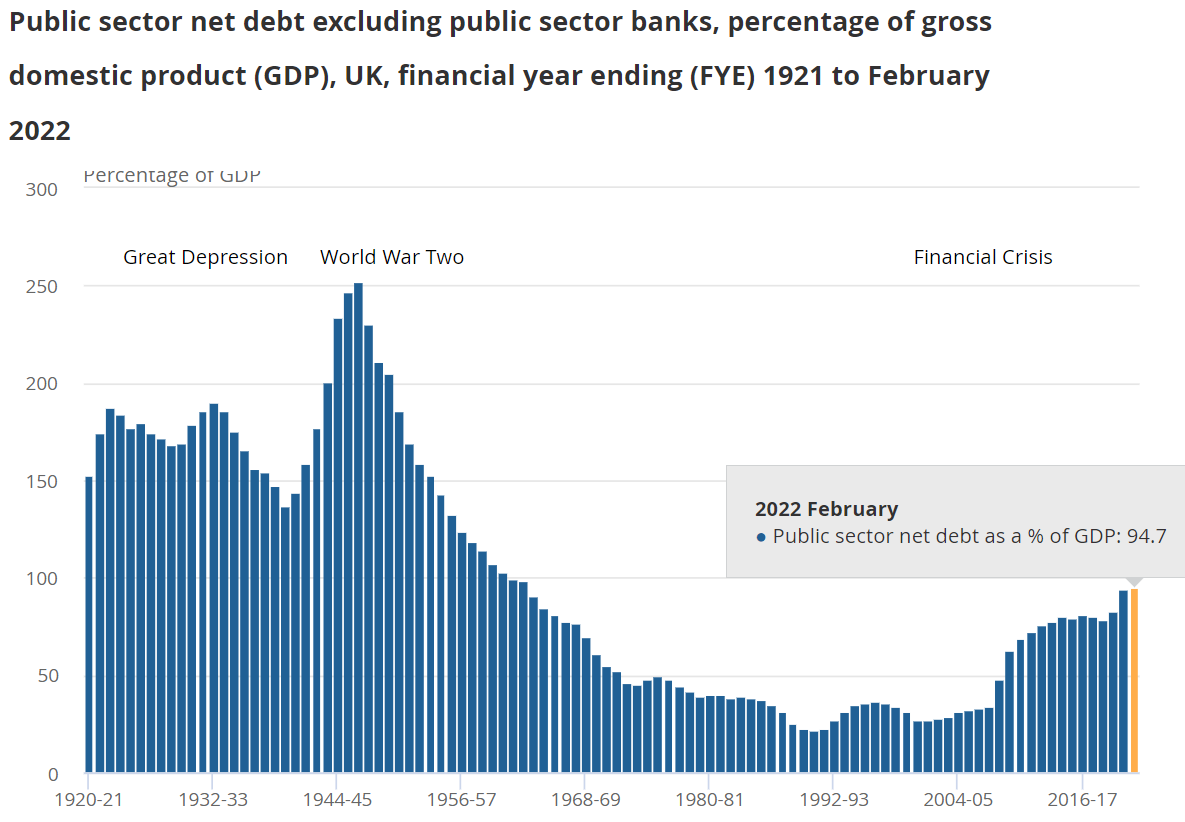

At the end of January 2022, public sector net debt, the headline statistic, was equivalent to around 95% of GDP, compared with 81% before the pandemic.

The OBR indicate that history suggests there is a better than 50/50 chance of meeting each of the Chancellor’s stated fiscal targets. For example, the fiscal mandate to have public sector net debt as a share of GDP falling by the third year of the rolling forecast period. These are met with a headroom of around £30 billion. Yet ironically few fiscal targets have been met in the past. With numerous risks to the current outlook at present, for example higher energy prices and inflation as a result of a longer war in Ukraine could be expected to reduce this headroom available.

The projected stock of debt, as a proportion of GDP, has been revised down by the OBR in all coming years of the projection. But while debt has been revised down, the higher likely path of inflation raises the cost of servicing the debt. Lower cumulative borrowing across the forecast means that headline net debt peaks as a share of GDP in 2021-22 at 95.6 per cent.

Fortunately, the OBR’s expectation from a year ago, of the headline rate reaching 110% of UK output (GDP) in 2023-24, has been defeated and the likelihood of debt exceeding 100% of GDP seems to be receding, for the present, albeit the peak will still be the relative highest since 1962-63.

Interest rates

If one recalls, the OBR pointed out last March, 2021, that in view of the scale of total historic public debt: “…debt interest may go from being a minor relief to a major headache for a Chancellor already trying to cope with the other post-pandemic pressures”.

The threat of inflation will have consequences, not only for households, but for the public finances too. The sensitivity to debt interest spending is almost twice as high as it was in 2014. The Chancellor seems to have perhaps recognised, in holding firm against calls for largesse, that the climbing costs of servicing the UK’s stock of debt can no longer be ignored - even at the risk to his own popularity.

After the US Federal Reserve made the first move to begin lifting interest rates it was all but certain that the Bank would increase Base Rate. The Bank of England’s Monetary Policy Committee (MPC) raised Bank Rate to 0.75% on 17 March, up from 0.5%. Between 19 March 2020 and December 2021 this had been at 0.1%, the lowest ever level. This was the third such meeting in a row where the Base Rate was increased.

The Bank is now playing catch-up with rising expectations of inflation that, should CPI touch 8% this April, will be well above the MPC’s 2% target. The MPC has also announced the reduction of the QE asset purchase programme from the peak value of £895bn.

Anthony Denny

9 April 2022